Get the most Tax Credit for health insurance in Texas

There's so much confusion around what is arguably the biggest source of help from the crushing cost of health insurance.

The Tax Credit or Subsidy for Exchange plans!

Let's make this all easy so that when you run your quote here, you can enter the correct information.

50% of people we help who enrolled themselves in the Exchange have errors that will prevent them from getting the most subsidy.

Or worse yet, they'll have to pay back some or all of it at tax time!

We want to avoid a tax bill of potentially $1000's to the IRS please.

First, our credentials:

>

Here's what we'll cover:

- A quick lay of the Tax Credit landscape in Texas

- What income to use for the subsidy

- What makes up a "household"

- How to quote Texas exchange plans with the subsidy included

- How the subsidy "settles out" at tax time

Let's get started!

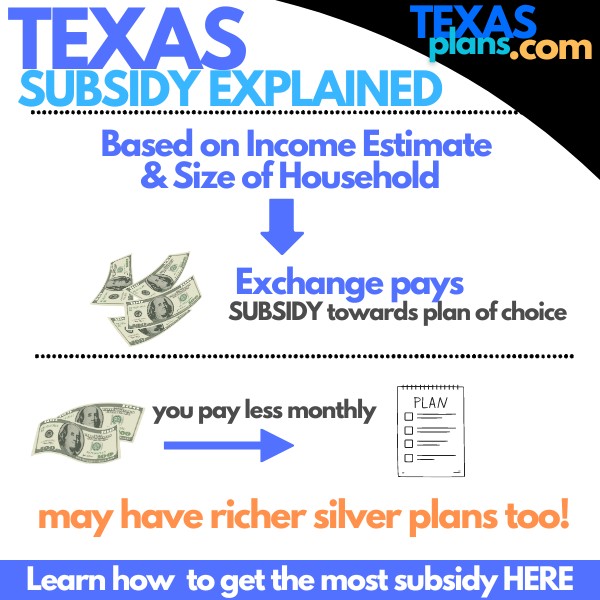

A quick lay of the Tax Credit landscape in Texas

Since 2014, there's a built-in subsidy for health insurance which can be sizable.

It's all based on income these days!

You get the subsidy right away so the amount will be deducted from your monthly insurance premium.

For example:

- Silver plan is $400

- Tax credit is $250

- You'll get a bill from carrier for $150/month!

This is just an example. We see subsidies that can eat up almost the full premium!

There is no longer a Federal penalty for not having health insurance but in case you've been asleep the last few years, this is not the time to go without coverage.

We're seeing bills with clients of $250K+ for hospital stays relating to heart and cancer treatment.

Plus, the best providers are going to ask you for the insurance card for treatment.

Back to the subsidy.

The amount you get is based on income and size of household. Let's zero in on these to make sure we're using accurate info.

This is a huge source of confusion on the market.

What income to use for the subsidy

If you have a more complicated situation, email us at help@texasplans.com or call us at 800-320-6269. You book a time to chat here.

Basically, we're trying to estimate our AGI (Adjusted Gross Income) on the 1040 for this year.

This means the income that we'll report in April of the NEXT year.

The past year doesn't matter...it's already in the books. We want to estimate THIS year's income.

That can be tricky for many people such as the self-employed or people in flux (changing jobs, etc).

Technically, the following are also added to the AGI but they're more rare:

- Foreign income

- Tax-free interest

- Untaxed Social Security

The AGI foots the bill for most people (probably 95%+).

You can look at your prior 1040 tax from if your income doesn't change much and zero in on the AGI.

Otherwise...

- W2 employees: Go with gross income estimate. Standard deductions don't apply for the AGI

- Self-employed: Focus on NET business income. Business income minus business deductions.

Again, this is where things get really tricky for many people so reach out to us at help@texasplans.com

Here's the income chart we whipped up to make things easier for you:

Next up, whose income??

What makes up a "household"

Household is defined as everyone that files together on a 1040 tax form for the period in question (this year).

This is true even if not everyone is enrolling. We still look at the full household income.

Luckily, our system will take this all into account.

Married people must file jointly to get the subsidy. You can't file separately with one spouse who has low income and get the subsidy that way.

It's the full household and filing jointly is required.

What about a household that is changing (marriage, divorce, new baby, etc)?

This is tricky.

We can go based on our situation at the time of applying BUT it will all settle out when we file taxes the following year based on our status 12/31 of the current year.

So...we could get a huge subsidy as a single person now. Get married in December to a spouse who makes a lot more money (casting no judgment!!) and then have to pay back that subsidy (or a portion of it).

Ideally, go based on how you expect to end up 12/31 so you don't have surprises OR just have some money stashed away to pay back when you file taxes.

There's no penalty per se...just the subsidy you weren't eligible for.

This may figure into what plan you pick though (going for bronze for example to keep costs down).

Alright, we have the two big pieces ironed out.

Now what??

How to quote Texas exchange plans with the subsidy included

We make this fast, easy, and free!

Run your Texas exchange plan quote here WITH subsidies built-in:

Make sure to enter your total # of household members (everyone filing together on a 1040 tax form) even if not everyone is enrolling.

We can run this quote for you as well. We just need:

- Dates of birth

- Zip Code

- Best estimate for this year's income

- Who is enrolling

Email us this at help@texasplans.com and we'll get to work.

Most importantly, we'll point out any good values in the mix as we know the

plans inside and out.

There's no cost for this quoting tool. The rates are the best available. Our assistance is 100% free to you.

How the subsidy "settles out" at tax time

This is why we went through everything above with you.

Let's say we think we'll make $30K for this year. We get a big bonus or something that increases that AGI to $50K.

Well...as soon as you know your income is going to be higher, we want to update that with the Exchange right away

This will immediately (next month) adjust your subsidy and how much your monthly premium is.

If we did this in say June, we would have been getting a higher subsidy for half the year (Jan - June).

We'll likely have to pay this back at tax time or our remaining subsidy will go down to reflect that we received too much.

It also works the other way!

Let's say we estimated $50K but our income actually came in at $30K.

In that case, we'll recoup the extra subsidy when we file taxes the following year!

We don't lose it. If we adjust the income mid-year (say in June again), we'll get more subsidy for the remainder of the year.

Net net...

It all comes out in the wash! No penalty but we'll either pay back subsidy (under-estimated) or recoup subsidy (over-estimated income) at tax time the following year.

Let's try to avoid any surprises either way and estimate as well as possible.

That's where we come in!

No cost for our assistance and we've run 10's of 1000's of these calculations for over 10 years now.

Lean on...it's zero cost!

Call 800-320-6269

Chat online here

Pick a time to talk here