Texas Health Insurance - How to Compare Cobra and Texas Obamacare

How to Compare Cobra and Texas Obamacare

We get this question almost daily from people losing employer coverage in Texas.

How do I compare Cobra and Texas Obamacare?

First, Obamacare is just a blanket term for any individual family plan whether on or off exchange.

They both have the same networks, rates, and benefits... with one big difference.

Subsidies on exchange which can bring down the cost significantly especially for people who have lost a job.

We'll explain more below but first or credentials:

This is what we'll cover:

- Quick intro to Cobra options in Texas

- How to compare Cobra and Texas Obamacare

- The Obamacare subsidy versus Cobra

- Comparing Cobra and Obamacare networks

- How and when to enroll in Obamacare from Cobra

Let's get started! There might be $1000's saved in the move.

Quick intro to Cobra options in Texas

First, a lay of the land:

Cobra is continuation of the employer plan offered to the employee after loss of coverage whether terminated or voluntarily quitting.

Only a few things can block Cobra options:

- The employer plan shuts down altogether

- You're eligible for Medicare (watch out for this one if age 65 or older)

- You were terminated for fraud or gross misconduct

You pay the full premium usually with an additional 10% added on.

Generally, there's a 60 day window from your last date of employer coverage to "opt in" for Cobra but go by the date you get on letter.

Cobra is super strict on this and payments. They will cancel if we don't meet deadlines!

The coverage is retroactive which means it will go back to the last date of coverage even if you elect Cobra later in that 60 day window.

For example:

- You're terminated May 15th

- Employer coverage ends May 31st (typical with employer plans)

- You have through July to elect Cobra back to June 1st eff date

- You'll have to pay the back premium for this period

You can cancel Cobra coverage month to month and it generally goes for 18 months. You may be able to change plans at the time of Cobra election if the employer offers different options but check with them.

Otherwise, the coverage will be same you had while employed. You're just paying the bill!

You can generally piece-meal Cobra meaning...

- Enrolling only certain family members

- Enrolling in only certain benefits (taking dental but not medical, etc)

If you have other questions about Cobra, check in with us at help@texasplans.com or 800-320-6269.

So...what's the alternative?

How to compare Cobra and Texas Obamacare

The main option to price-check against Cobra is Texas Obamacare.

This basically refers to individual family plans whether on-exchange or direct with the carrier.

These days, most enrollment (99%ish) is on exchange and here's why:

- There can be huge subsidies that reduce the cost of coverage based on income (which probably just dropped, right??).

- We have big reviews on Texas Obamacare and how to pick the best Obamacare Texas plan.

But let's hit the highlights:

- After 2014, individual family plans are very similar to employer plans in what they cover

- You can't be declined based on health

- There's no waiting period for pre-existing conditions

- Core benefits are now mandated for individual family and employer plans

- Rates are now pretty similar between the two UNLESS you qualify for a subsidy

The subsidy really is the big deal on the market and we'll cover that next section.

Where are they different?

- The networks on employer plans tend to be bigger and there are still PPOs (more on that below)

- Cobra plans may have added benefits (fertility, etc)

- Cobra plans may have access to nationwide networks depending on how they're structured

So...really, it's cost (if we get a subsidy) versus network size and flexibility for the most part.

Let's then break those down.

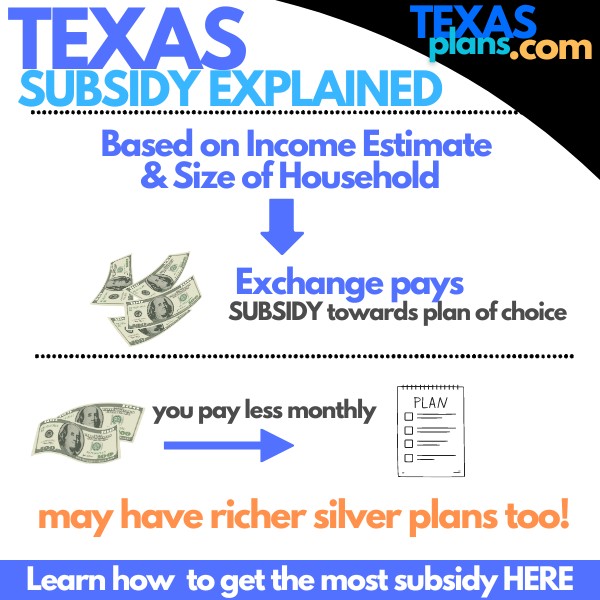

The Obamacare subsidy versus Cobra

First, let's tackle the "cost" side of things:

With Obamacare, if our income is within certain ranges, we can get large subsidies to reduce our monthly premium.

Income is defined as:

- Our estimate for this year's AGI on the 1040 tax form; next April's filing

- Household is everyone that files together on a 1040 tax form; even if not enrolling

This is where people get really mixed up especially when income is in flux (losing job).

We're happy to help at zero cost to you: call 800-320-6269 or email us at help@texasplans.com

It can be really confusing if our annual estimate is different from what we're making right now (including unemployment) so check in with us to make sure we don't miss out on subsidies.

Big reviews on how to get the most out of Texas health subsidies and the Income chart for Texas Obamacare.

General rule of thumb:

If we're under the 300% range, we're probably looking at pretty subsidies.

We can even get much richer versions of the silver plan under the 250% level.

As we get older, the subsidy goes up quite a bit so check your quote here:

We're happy to run it for you with zip code, dates of birth, and income estimate.

It's not unusual to see Cobra rates of $700 and Obamacare rates half that if not less.

So...what's the trade off?

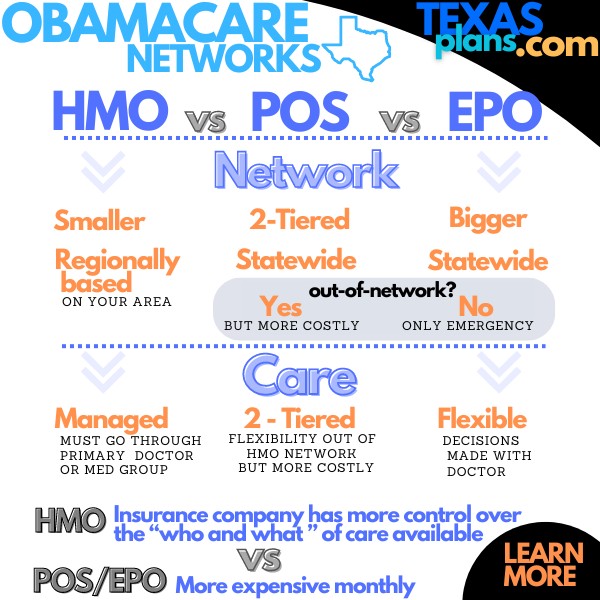

Comparing Cobra and Obamacare networks

As we mentioned, Cobra networks tend to be larger than those of Texas Obamacare plans.

There's also been a move towards the HMO side of things on the individual family markets with a few EPOs sprinkled in.

EPOs work like PPOs but you have no benefits out of network other than a true emergency.

Employer plans can still have PPOs but you may pay dearly for it.

How do the employer PPOs compare to the EPOs on exchange?

First, check out your doctors in the quote tool below to see if it's even an issue.

Otherwise, the out-of-network benefits for PPOs these days are nothing to write home about.

The carriers keep watering down how much they'll pay out-of-network providers to where you really want to stay in-network, even on a PPO!

We've been on EPOs and PPOs before and they feel pretty comparable.

Again, the best plan is to see if your doctors and/or hospitals are in network through the quote tool.

Speaking of which...

How and when to enroll in Obamacare from Cobra

We make this free, fast, and easy here:

A few notes.

If we start Cobra and are outside the 60 day window from losing coverage, we likely can't get Obamacare until open enrollment (Nov 1st - Jan 15th) or a special enrollment trigger.

See our guide on when you can enroll in Texas Obamacare.

As we mentioned above, income estimates based on:

- AGI on the 1040 tax form for this year; next April's filing

- Household is everyone on that 1040 even if not enrolling

Look...this stuff gets confusing so reach out to us for free assistance comparing Cobra and Texas Obamacare.

Help@texasplans.com or call 800-320-6269.

There's zero cost for our assistance and if your Cobra option is better, we'll tell you so. We do it everyday.