Texas Catastrophic Health Insurance Plans Explained

We get this call daily and people generally mean a few different things when they're asking for catastrophic health coverage.

The loose translation is... "I want the cheapest coverage for just the big bills"!

That means very different things since 2014 with the ACA law in effect but we do have at least 3 different options to address this need.

We'll cover the pros and cons of each below but first, our credentials:

Here are the topics we'll cover:

- Why catastrophic health insurance can make sense financially

- Double-checking the subsidy with exchange coverage

- The Bronze level plan for Obamacare

- Short term health plans including Hospital only from United

- Health Sharing plans in Texas

- Which catastrophic Texas plan is best

- How to quote and enroll in Texas catastrophic coverage

Let's get started...lots to cover.

Why catastrophic health insurance can make sense financially

We no longer have the Federal penalty for being uninsured so we're back to the basics of why get insurance at all!

It's about covering the big bill so that you're on a multi-decade payment plan to the local hospital.

Yes, you're healthy but since Covid, we've seen so many unexpected claims for heart and cancer at 100K+ that we've given up counting. Even young, healthy people in their 20's.

It's the wrong time to take this bet:

The other thing people without coverage don't realize is the first question you'll get at the hospital is..."Can I see your Insurance card?"

How you answer that may lead to very different outcomes in terms of where you get care and what's available.

So, catastrophic coverage is much better than having no coverage and may make financial sense anyway as long as it's legit coverage.

Essentially, it's about covering the big bill at the lowest premium.

There's another factor most people don't realize since 2014 that high favors catastrophic coverage.

The plans are all guaranteed issue now which means you can't be declined based on health.

As a result of this and a decade of gaming the system, you'll find that each step up in plans (say from bronze to silver, etc) costs you in premium about what you might get in benefits!

We remember early on where people would call in and say..."Give me the platinum plan...I'm getting my knee replaced".

That eventually figures into the pricing and voila...the platinum costs you that much more in premium!

So going down the scale has always made sense, especially if we're older where the premium different more than makes up for the benefit difference.

One secret on the Obamacare plans...

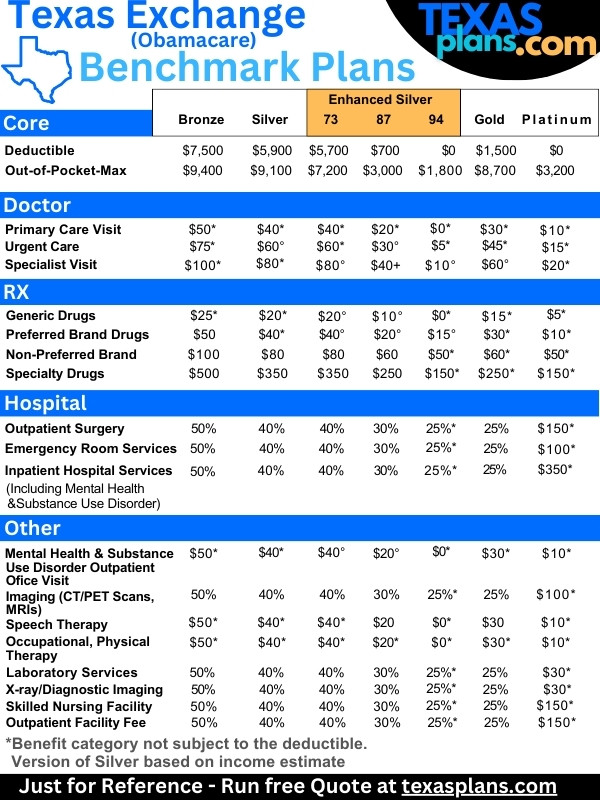

The Out-of-pocket max (your protection from big bills) is roughly the same for the bronze, silver, and gold plan!

Even more reason to go down the scale if the premium savings pays for it.

Let's look at the hierarchy of catastrophic Texas health plans from best to worst as we'll see below.

First, we need to see if we qualify for a subsidy.

Double-checking the subsidy with exchange coverage

This is really the biggest deciding factor on health insurance cost and so many people get this wrong on their own.

Based on income, we can qualify for big subsidies that are paid towards our chosen health plan, even, the lowest level bronze plans.

This subsidy goes up as we get older and as income come down. Learn more on how to get the most subsidy but here's a quick chart.

- Estimate this year's income as the AGI on the 1040 tax form; next April's filing

- Household is everyone that files together on a 1040 tax form even if not enrolling

This gets confusing fast for many people so reach out to us (free service) at help@texasplans.com or 800-320-6269.

Again, we can apply the subsidy to the lowest bronze level plan but there are very rich versions of the silver we may be eligible for based on income as well. Check out the Texas enhanced silver plans.

With the full ACA (Obamacare) plans, the Bronze is the closest to catastrophic that we have.

Let's start there.

The Bronze level plan for Obamacare

The bronze is the lowest level outside of a special "Catastrophic" option for people under age 30.

One note...if we're eligible for a subsidy based on income, it will apply to the bronze but NOT the catastrophic option (under age 30).

For this reason, we almost always go bronze these days.

Here's the standard plan basis from which carriers can differ by 2% up or down.

It's pretty straight forward:

- High deductible around $7500

- Out-of-pocket max around $9400

- Copays for RX and Office visits may be subject to main deductible

This is pretty much...catastrophic coverage!

You can quote these plans WITH subsidy calculation here:

Why doesn't it fit the bill for many people in the market for catastrophic plans?

The ACA or Obamacare has basic requirements of what health plans MUST cover.

Including:

- Pre-existing conditions

- Pregnancy

- Medication

- Mental health

And much more. These come with a cost...especially the pre-x. Underlying health plan costs have roughly tripled since 2014 as a result.

If the subsidy above offsets this, we're usually okay which is why that's the first thing to check out.

Otherwise, the bronze is lowest priced option for comprehensive (Obamacare) coverage.

There can be HSA qualified plans at the bronze level as well which offer the ability to have a tax write-off off money funded in a separate HSA account which can be used to pay medical/dental bills pre-tax.

We're happy to walk through this option with you.

What if we want to scale down things even from there or can't enroll on Obamacare plans (missed open enrollment, etc)?

Short term health plans including Hospital only from United

Short term plans mirror what we used to have before 2014 and the ACA law went into effect.

- Waiting periods for pre-existing conditions

- Does not cover pregnancy

- Some plans just cover hospitals and surgery

United Health dominates the Texas short term health market and we have a full review there.

You can quote it here:

They have 4 basic options with increasing benefits:

- Hospital and Surgical - catastrophic care for facility based needs

- Tri-Term Value - adds in other benefits (office, etc) after deductible is met; RX card

- Copay Select Max - adds in copays for office and RX; coinsurance up to max after deductible

- Plan 80 Max - you pay up to deductible then plan takes over for covered benefits

What really makes these options more catastrophic in nature is the choice we have in how the plan is structured.

We have control over a pretty wide range of:

- Deductible - amount you pay first before the plan kicks in

- Coinsurance - % you will pay after the deductible up to the max

We recommend focusing on the out-of-pocket max since $20K can be a huge bill if something comes up.

Catastrophic shouldn't mean you can't afford healthcare costs even with insurance!

Reach out to us with any questions but we give a full walk-through how to compare the Texas short term options.

It's not as robust as the Bronze plan with Exchange plans but still has a solid carrier and network.

In Texas, having such a strong short term health plan option has made the next entry less attractive.

Health Sharing plans in Texas

In some other States, they've banned short term so this is our only option if we've missed open enrollment or just want catastrophic.

In those cases, we've used OneShare since it's the most flexible in terms of eligibility but we prefer United health over this option in Texas.

Health sharing plans are memberships. They're not health insurance plans. The biggest issue we've seen (aside from the blowing up over the last few years) is that hospitals have become pretty negative to work with them.

They'll ask you for your insurance card as we mentioned above and if you have a health sharing company, good luck with that. It gets pretty choppy real fast!

This is the last thing you want to deal with when scheduling chemo or bypass surgery.

Again, United's short term is a much better option for actual health insurance if we just want the lowest cost option and it can start midnight after enrollment.

So in Texas, health sharing plans don't really make sense. We're happy to compare the two for you.

So...how do we compare these options?

Which catastrophic Texas plan is best

It's pretty simple really. Follow these steps.

Do you qualify for a subsidy based on income estimate (learn more here or reach out to us at help@texasplans.com )

If so and it's pretty big, that's hard to beat. Go with the bronze or maybe even silver depending on how much subsidy and if you're eligible for the silver plans.

A guide on how to compare the Obamacare metallic plans.

If you don't qualify for a subsidy, what is the bronze plan cost like? Too high?

Okay then look at United Health's short term plans here.

Pricing wise, where are you comfortable.

Absolute bare bones is the Hospital and Surgery but we would rather have richer plan with higher deductible.

Trying to guess what health care you'll need (or not need) is not that different from trying to guess whether you'll have any health issues at all.

Really, those are the legit catastrophic options available in Texas for actual health insurance.

Be wary of anything outside of these as a cheap monthly is basically worthless if it's not going to come through when needed.

Throwing good money after bad and if you've read this far, you're trying to save money...not risk it.

Again, our goal is to protect from $100K+ medical bill at the lowest cost available.

After all, that was the original intent of health insurance before it became expensive nickels and dimes.

Alright...what are the costs for these options?

How to quote and enroll in Texas catastrophic coverage

We provide quotes and online enrollment for all options here:

The Obamacare quote will show you the subsidy based on income and size of household. Check out how to get the most out of the subsidy but...

There's zero cost for our assistance and we help people with the income question all day long.

help@texasplans.com or 800-320-6269. Pick a time to chat here.

There are specific times we can enroll in Obamacare plans so reach out to us with your situation (loss of coverage, move, life changes, etc).

Short term can start anytime during the year. Those plans can only go 360 days so reach out to us on a little dance we do during open enrollment to make sure you don't have a lapse in coverage.

We're here to help as you can see from the reviews!