Why Didn't I Get a Tax Credit on Texas Health Exchange?

Most people will take a look at our income chart for the subsidy and wonder why they're not getting any help.

Keep in mind that roughly 50% of people who self-enroll have mistakes on the app (it's complicated) which might prevent them from getting the full subsidy they're eligible for.

We'll walk through the common errors but definitely use us to have a second pair of eyes over the enrollment. There's just too much.

Here's are credentials:

This is what we'll cover:

- Common reasons people don't get the full Texas health subsidy

- Not getting Texas exchange subsidy due to income

- Household and tax filing issues for Texas health subsidy

- Other Texas health exchange eligibility issues

- Medicaid blocking subsidy for Texas Obamacare

- How to fix Texas health exchange account

Let's get started!

Common reasons people don't get the full Texas health subsidy

This is only a top-level review as people's situations are varied and complicated!

After enrolling 10's of 1000's, we've seen it all since 2014.

Let's walk through the common issues that keep people from getting the best subsidy:

- Income below the 100% level

- Income too high and not using the correct income

- Married but filing separately

- Not legally present in the US

- Medicare eligible

- Incarceration status blocking it

- Medicaid and/or CHIPs is blocking enrollment

These are the big ones but there are lots of other quirks in their enrollment system that can cause issues.

Just answering one question wrong can rock the apple cart!

Reach out and get help for no cost here:

Even with existing Exchange accounts.

In many cases, a person is getting a subsidy but not nearly what they're eligible for due to the complexity of rules. Especially around income.

So let's get into the above items in more detail along general groupings.

We'll start with everyone's favorite. Income.

Not getting Texas exchange subsidy due to income

Income is so tricky in this whole calculation and we spend about � our times these days fine-tuning the income estimate.

What used to be about picking health insurance has basically become a tax issue now!

We go deep into here:

- How to get the most Texas health subsidy

- Income chart for the Texas Obamacare subsidy

- What income is included for Obamacare in Texas

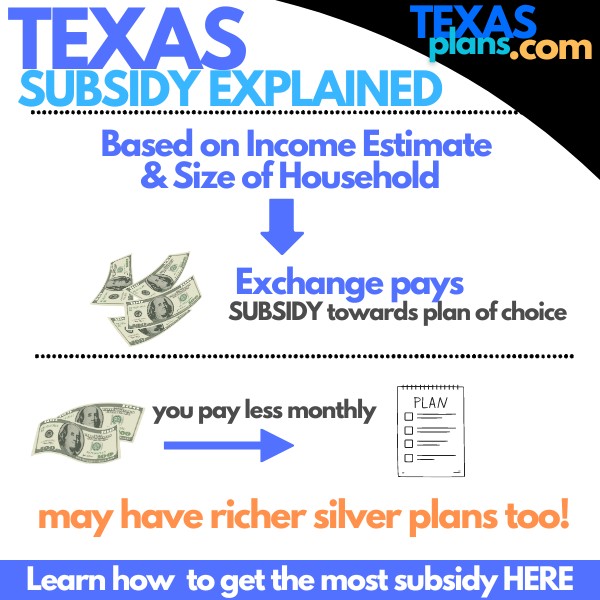

First, understand that our income estimate is probably the most important piece now in dictation how much we'll pay for insurance.

We could be talking about $1000's per year!

There are a few ways that income issues can cause us to get no subsidy or less than we're eligible for.

First, if our income estimate (for this year) is below the 100% level on the below chart, we're likely in the medicaid range.

We have to meet other requirements (see Lost medicaid and need Obamacare) as well but income is part of the equation.

So...let's say our income estimate is $15K and we don't meet the other requirements (usually pregnant and/or disabled).

We get no subsidy! Nothing. It's brutal since these people are exactly who the ACA was designed to help.

Reach out to us if you're below 100% on the below chart so we can make sure we're using the right numbers.

Then there's an issue the other way!

What if our income is too high? The subsidy operates on a sliding scale so above 100% on the chart (minimum income for subsidy), it will go down as our income estimate goes higher.

This can vary depending on age believe it or not but generally speaking, the income starts to really drop off around the 400% level (unless we're in our 50's and 60's).

The law basically says that our share of premium should cap around 9% of our income.

If we're a single person making $100K, we may not see much subsidy unless we're much older.

That's why getting the right income estimate is so important and it's important to get a second pair of (seasoned) eyes on the numbers here.

Even the household make-up is confusing under their rules so let's touch base:

Remember, last year's income doesn't matter. We want to estimate what we'll fill for the AGI on the 1040 tax form for the year we're being insured (what will show on filing the following April).

Then, there's issues with the definition of "household" and tax filing.

Household and tax filing issues for Texas health subsidy

Their definition of household is everyone that files together on a 1040 tax form for the year we're being insured.

This is usually the tax filing the following April.

A few key notes here that can prevent the subsidy.

If we're married, we have to file jointly to get the subsidy. If we file separately... no subsidy!

It's just the rules in the original ACA law.

Otherwise, loss of subsidy usually comes from big changes in the household (marriage, divorces, etc) that suddenly group different income streams together.

It's now based on the "household" income which has changed. Again, let's walk through the specifics as it can get complicated.

For example, one fiancee may have very low income (and a subsidy) while the other fiancee has high income (no subsidy and/or employer coverage).

After marriage, voila! They're a household of 2 and must file jointly. The new "household" income reduces the subsidy for the person who had lower income before marriage.

Now add to this all sorts of other changes (divorces, births, deaths, job changes, moves, etc) and you can see how it complicated fast.

Also, we have to file taxes in order to get a subsidy. It's just a requirement so they have something to compare against. That's for the year of coverage.

Outside of taxes and income, what else generally causes issues?

Other Texas health exchange eligibility issues

There can be other questions that make us ineligible for the subsidy.

The most common are:

- Showing as incarcerated in the system

- Eligible for Medicare (even just Part A)

- Eligible for "affordable" employer coverage (see dropping employer coverage and getting Obamacare)

- Not a legal resident in the US

The employer "affordable" coverage issue trips people up quite a bit. If a person is eligible for a subsidy, Texas exchange plans might be much less out of pocket than the employer plan.

The issue is an employee's share of employer plan premium has to be more than 8.39% in order to qualify for a subsidy.

If the employee's share (self and/or dependents) is under that, we can't get a subsidy.

Many employees are dropping job plans to get Texas Obamacare and even many employers are dropping group plans so their employees can avoid this "affordable" issue which prevents higher-paid employees from getting a subsidy.

We look at Texas employer dropping group plans but this requires some discussion on both ends.

Reach out to us if you're not eligible for the subsidy and can't tell why.

We can even help with existing accounts as certified agents and there's zero cost for our assistance!

One more big one that comes up often.

Medicaid blocking subsidy for Texas Obamacare

It's pretty often that someone will apply for Texas Obamacare and the final screen comes back with... no subsidy.

They're in the right income range so what gives?

There may be an old Medicaid enrollment that's essentially still active. It's in the system and blocking enrollment since you can't be eligible for Medicaid AND a subsidy.

That needs to be cleared out first and then we can get you enrolled on Obamacare with the full subsidy.

It usually means updating the income with Medicaid and requesting them to release the account so we can enroll.

Technically, this is a loss of coverage and gives us a special enrollment trigger outside of open enrollment.

We can guide you through the process.

So...this is a lot of information on a topic that was already confusing? Help!!!

How to fix Texas health exchange account

The fix depends on what the issue is.

We can help with existing Federal exchange accounts to quickly figure out what's causing the issues as there can sometimes be many.

Just contact us and we'll get started with full details on how to navigate the fix as quickly as possible.

There's zero cost for our assistance as certified Texas exchange agents.

When we help people enroll newly (access Texas health exchange application), we scrub the application first before processing on the Exchange just to prevent these sorts of issues.

We'll also notice if you're really close to richer Silver plans (see silver 87 and 94) or other benefits to you.

It's complicated now. The outcome can involve $1000's out of pocket. Get help!