I want to offer my Texas employees Obamacare

There's been a big transition over the last 10 years and it's only accelerated since Covid and the following inflation that is pounding small Texas businesses.

Many employers are either canceling their employer health plans or working to help employees get Obamacare in Texas.

We already looked at whether an employer should cancel their group plan for Obamacare but let's explore how exchange plans work for employees.

If done correctly, it can mean much less expense for employees and even the employer!

First, our credentials are here:

This is what we'll cover:

- Can an employer offer Obamacare to employees in Texas

- Comparing employee benefits versus Texas Obamacare

- Using ICHRA to help employees pay for individual plans

- What type of companies does Obamacare work best for

- How to quote and enroll on-exchange for employees

Let's get started!

Can an employer offer Obamacare to employees in Texas

Technically, there are two completely separate markets:

- Small business: 1-100 employees where the plan is "hosted" by the employer

- Individual/Family: individuals plans purchased by the employee

There is an actual small business Obamacare plan available for companies to offer and there may be subsidies depending on the average salary of employees, size of company, etc.

These subsidies are temporary so this hasn't been that popular since 2014 when the law went into effect.

Mainly, employers are calling us and asking about helping their employees with the Exchange for personal individual/family plans.

That is a separate situation all together in which the employer doesn't really interact outside of the ICHRA setup which we'll discuss below.

Really, the employee is purchasing a private health insurance plan for them and their family and it's separate from the employer in this situation.

This has been the trend over the past years and it's only speeding up.

Where we still see traditional employer sponsored plans is with professional and high-end industries where securing talent is very competitive.

It's more a benefit or perk of employment that needs to be offered to attract the right employees.

So...this decision of offering employer-based health plans versus allowing employees to get Texas Obamacare depends on the industry.

A good rule of thumb is to look at average annual salary. Why?

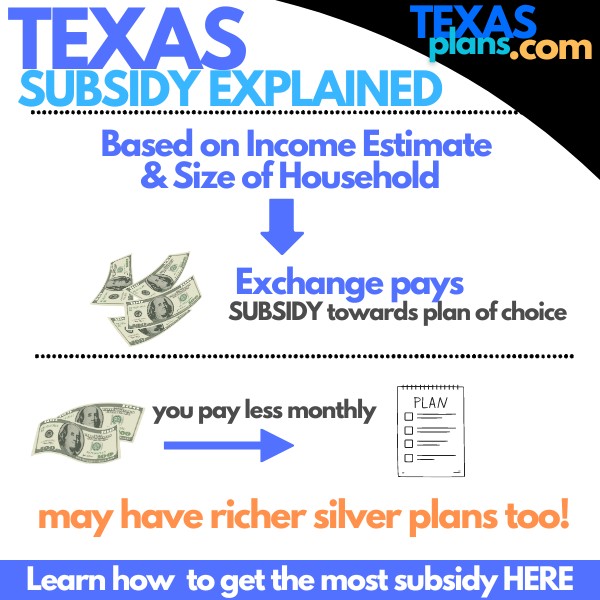

Because the big draw of the on-exchange Obamacare is the subsidy which brings down monthly cost and it's based on income estimate for this year!

Let's look at this and the other differences.

Comparing employee benefits versus Texas Obamacare

We'll evaluate the three big considerations (outside of attracting/keeping talent):

- Benefits

- Networks

- Costs

First, benefits since it's the easiest.

Generally speaking, the plans on the small business and on-exchange markets are standardized and very similar.

A silver plan is going to walk and talk like another silver plan across both markets +/- 2%.

This makes it very easy to compare.

The other big protections are the same now:

- No waiting period for pre-x

- No declination based on health

- No lifetime or annual max benefits

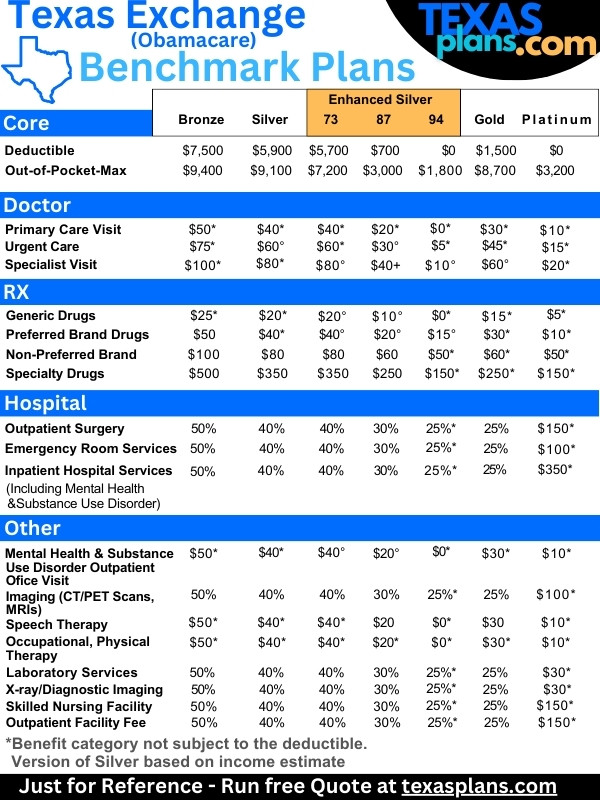

The same mandated benefits are covered now. More on how to compare the metallic plans and here are the benchmark plans:

Where there is a difference can be in the networks...which doctors/hospitals you can see and how care is managed.

Network difference between Texas small business and individual/family

Generally speaking, the networks are smaller and more on the individual market.

Employer plans can still have PPO plans and we looked at how some family businesses get employer plans to have a PPO.

The individual/family market is mainly HMO now with some EPOs sprinkled in. We looked at the Texas Obamacare networks in more detail.

The way to address this is to run your quote below and check the provider finder to see who works with your doctors.

As for how care is managed, learn about the differences between EPO and HMO here.

Let's turn to the real reason people are switching to on-Exchange...It's all about the cost!

Cost difference between small business and on-exchange in Texas

There can be a huge subsidy on-exchange which brings down the monthly cost to employees.

Depending on income, we see costs down to zero each month!

More on what income below in the quote section but here's the income chart to get a sense of the numbers:

Let us help you evaluate the potential savings for employees and take the guesswork out for you.

So, not only is the employer saving on group plans but employees may be getting massive help from the government towards their choice of coverage.

If they're in the sweet zone (100% - 250% on the chart above), they can also get richer versions of the silver plan for the same cost. More on the enhanced silver plans.

We find many employers are unaware that their employees are missing out on these really rich plans (sometimes richer than the platinum plan) at reduced costs (because of subsidy).

The employees end up much happier with a lot less out of pocket. Look at the difference in max-out-of pocket in the standardized benefits:

If an employee or their dependents has a major health issue (all too common these days), it can mean $1000's out of their pocket on the backend.

See why employers are moving this way!

Let's look at a tool that's come on the scene since 2020.

Using ICHRA to help employees pay for individual plans

Basically, ICHRA provided a means by which employers can contribute pre-tax towards employee's individual family plans.

Here's the rub...any amount the employer contributes reduces the subsidy from the government equally.

So...why do this at all?

Generally, this makes sense when employers have employees that make more money and won't qualify for much subsidy.

It's a way to still help employees on the higher end.

An employer may also increase wages but it can't be to "compensate for individual/family health plan premiums".

Has to be kept separate but since the on-exchange enrollment is exploding these days, an employer that is able to offer higher wages can attract better employees and still not be at a disadvantage by not offering ICHRA or employer-sponsored coverage.

Just remember the health plan is a separate issue.

You can instruct them to reach out to us and we'll help them through the whole process to get enrolled and qualify for the subsidy but it's separate from the employer.

So...who does this work well for these days?

What type of companies does Obamacare work best for

Really, it comes down to average income levels.

Looking at the chart above, an individual making between roughly $22K and $36K will probably qualify for a pretty solid subsidy and the richer silver benefits.

As a person gets older, the subsidy tends to go up as well.

There's currently no hard cap but the law basically says that a person's contribution shouldn't be more than just under 10% of their AGI income estimate.

Meaning...if a person makes $4K per month, their healthcare share should cap just under $400/monthly.

You'll get exact subsidy estimate in the quote section below.

What we see is that older people (40-64) tend to subsidies even at higher income levels!

Again, have employees run specific quotes for themselves and we'll guide them through the whole process.

There's zero cost for our assistance with 10's of 1000's of on-exchange enrollments under our belt.

help@texasplans.com or 800-320-6269 or pick a time to chat here.

This means that 100's of 1000's of Texas small businesses will benefit from this setup and avoid the complaints they see annually with small business plans.

It really removes a source of irritation between employer and employee especially if the subsidy and richer silver benefits kick in.

So...how do we make sure we quote this correctly?

How to quote and enroll on-exchange for employees

We make this fast, free, and secure here:

A few notes to get the most accurate quote:

- Income is estimate for the AGI on the 1040 tax form; next April's filing

- Household is everyone that files together on a 1040 tax form, even if not enrolling

Income is where we spend all day helping people since it's so confusing. Reach out to us with your situation and we can nail it down in about 5 minutes...Tops!

Enrollment is super easy as well but there are special rules on when we can apply so let us know what the employee's situation is.

Losing other coverage in last 60 days is a big trigger outside of open enrollment. Being between 100% - 150% on the chart above is another key one.

Again, let us know the employee situation. If an employer is canceling group coverage, that makes it easy since it's a loss of coverage!

We're happy to help with this whole process and make it easy for you and your employees.

help@texasplans.com or 800-320-6269 or pick a time to chat.