Texas Health Insurance for Self Employed Guide

There's enough weighing on the self-employed these days with costs spiraling.

We might actually have some good news on the health insurance front.

Being self-employed can be a huge advantage since 2014 on the new ACA marketplace (on-exchange).

We typically see $1000's in subsidies for self-employed people in Texas.

First, our credentials here:

This is what we'll cover:

- Intro to health insurance for Texas self-employed

- Figuring out the income and subsidy piece for self-employed

- The tricky piece with self-employed income and Obamacare

- What plans work best for self-employed

- How to quote and enroll in health plans for Texas self-employed

Let's get to it!

Intro to health insurance for Texas self-employed

First, let's define self-employee since some people miss out on benefits of being so.

Basically, self-employed people file as the following on their taxes:

- Sole-proprietor

- LLC members

- S-corp with pass-through taxation

Many times, they're paid 1099 which essentially means self-employed from the IRS' point of view.

The alternative is W2 which means employees.

Most other income is self employed income if ACTIVE (as opposed to investment for example).

Most self-employed people need to get their own insurance and there are two ways to do that in Texas but there's a clear winner.

Everything individual and family is called ACA (Affordable Care Act) or Obamacare. This is true for on or off-exchange.

Same rates,benefits, and networks. Learn all about general layout of the Texas individual family market.

Here's the key part for self-employed Texans.

On-exchange, we can get subsidies based on income and that's where the self-employed really benefit!

Let's get into why since this is THE big deal on the individual family market.

Figuring out the income and subsidy piece for self-employed

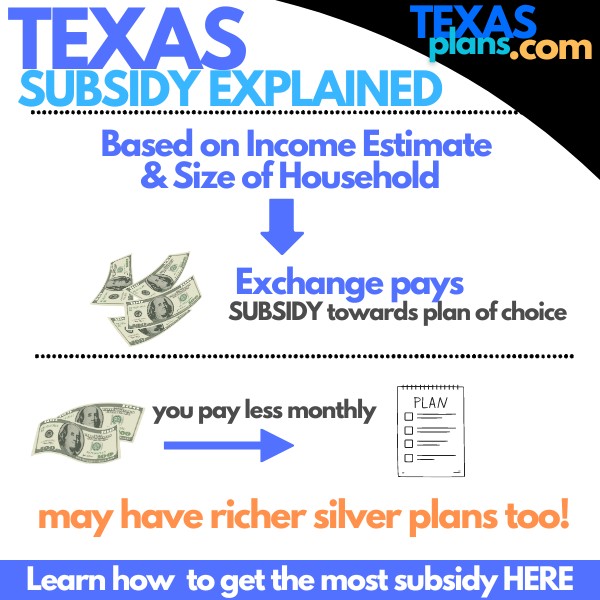

It all comes down to subsidies.

The subsidy is amount paid towards your plan choice on-exchange online which brings down the cost.

If you're paid W2, you have to list gross income.

Meaning, if I mean $50K on a W2 in a year, that's the number I have to go with.

Here's the good news for self-employed.

We can go with net business expense!

This means your gross self-employed income MINUS business expenses.

Both W2 and self-employed income drop down into the AGI on the 1040 tax form which is what we're trying to estimate for THIS year (next April's tax filing).

Last year's income doesn't matter. It's this year's AGI (next April's filing) that we're trying to estimate.

If you look above the AGI on the 1040 tax form, you'll notice that there are other deductions which can come off.

The two most common we see with self-employed people are:

- Health insurance premium

- 1/2 of the self-employment tax

These both reduce the net business income and mean we may qualify for more subsidy!

So...

- Take your gross self-employed income

- Subtract estimate for business expenses

- Subtract estimate for health insurance and 1/2 of self-employment tax

This is a pretty good estimate for most people. Look at your past 1040 to see what shows "above the line"...over the AGI.

Other incomes can add to self-employed income including:

- Capital gains

- Tax-free interest

- Foreign income

- Untaxed Social Security

- W2 of course

Here's why self-employed fare so well with Obamacare.

A self-employed person might make $50K (like the W2 employee above) but have $20K in business expenses.

Now, the number we're using for the AGI might be $30K!

Much more subsidy than the W2 employee with $50K.

Run your quotes here to see how you're looking:

Household is everyone that files together on that 1040 tax form, even if not enrolling.

Another big give-away to the self-employed is around the premium itself.

Health insurance premium is generally 100% deductible to self-employed as long as you have net income to deduct it against.

This can result in a huge reduction in the AGI which means...more subsidy!!

We spend most of our time helping people figuring out the income piece and this is especially true for the self-employed.

Here's question we get most often...

"I have no idea what my net business income will be for the full year. What should I do?"

Let's look at what happens if we estimate high or low.

The tricky piece with self-employed income and Obamacare

Estimating income a full year is brutal for many self-employed.

Most don't have an idea of the NET income till file their taxes the following April. Retail is a perfect example and real estate agents can see prospects change overnight with a big sale.

So...what happens if we estimate wrong? Is there a penalty?

First, if we get a sense during the year that our income is going to change (up or down) from our estimate, just let us know at help@texasplans.com and we can we update it in the system.

Otherwise, it all settles out at tax time.

Meaning:

- If estimate is lower than actual AGI, we'll have to pay back subsidy we weren't eligible for

- If estimate is higher than actual AGI, we'll recoup the extra subsidy

This all happens in April or when we file our taxes.

There isn't a penalty per se. Just the subsidy needs to match.

We don't want a big surprise (to the downside) at tax time so it's best to dial in the estimate.

Email us at help@texasplans.com or call 800-320-6269 for free assistance on this front.

Again, to get any subsidy, we have to enroll on-exchange (more on that below).

Let's make a quick detour to the plans.

What plans work best for self-employed

The subsidy applies to all the plans but what plans tend to work best for self-employed?

First the basic rules apply and we go through how to really compare the Obamacare plans.

Are there certain plans that really work for self-employed?

First, the benchmark plans:

Let's walk through some specific options:

- The enhanced silver plans

- HSA qualified

- Major medical options

Let's walk through these.

The enhanced silver plans

It's not just the subsidy. Based on income, we may also qualify for enhanced versions of the silver plans.

If you qualify for the silver 87 or 94, there's no reason to go any further.

They're almost platinum level plans for the same price of the silver!

You can go down to the bronze but any health issue that pops up will probably pay the premium difference between the bronze and these really rich silver plans.

We can help you compare them and make sure you're not right on the income line to qualify but missing out.

More on the enhanced silver plans.

HSA qualified for Self Employed

There's a version of the bronze plan that allows you to fund a separate tax-favored account

We have a big review on HSA plans in Texas but why it matters for self-employed.

First, many self-employed are trying to keep costs down and looking for more catastrophic type plans.

HSAs are usually bronze level plans which are the cheapest available plans. We can still apply any eligible subsidies towards these plans.

More importantly, if you look at the 1040 tax form, you'll see one of the deductions above that line is HSA contribution.

If you fund $4K (as an individual or double if 2 or more), that reduces your AGI which means you have more subsidy!

On top of that, it may kick you into an enhanced silver plan which can mean much richer benefits.

We can look at all of this for you but if a high deductible, bronze plan is a good fit for you, we like the HSA version of it versus the standard bronze.

Speaking of which...

Major medical options

Major medical loosely translates as "I want the cheapest plan on the market".

Two ways to do this.

The bronze plans we mentioned above. Otherwise, short term plans in Texas are the only thing that reflects what we use to have for major medical.

These are generally used when we can't enroll in Obamacare plans because we missed open enrollment OR we don't qualify for a subsidy and really can't afford the bronze plans.

Short term tend to be cheaper although they don't cover everything ACA plans cover or have the different protections.

Learn more about Texas short term plans.

We have a big review on Texas major medical health insurance which compares these options in more detail but here's the short list:

- Do you qualify for a subsidy? If so, Obamacare is the better bet

- Can you enroll in Obamacare right now? (Open enrollment or Special triggers). If not, short term may be the only option.

- Do you really want the lowest priced option available with very high exposure or hospital only? That's likely short term but we would rather have full coverage

Lots of moving pieces here so reach out to us. Zero cost for our assistance!

help@texasplans.com or 800-320-6269.

Let's look at those rates now.

How to quote and enroll in health plans for Texas self-employed

We make this fast, easy, and free here:

Remember:

- Income is this year's AGI estimate on the 1040 tax form: next April's filing

- Household is everyone that files together on a 1040 tax form, even if not enrolling

We're happy to help with all of this.

You can quote short term health plans in Texas here:

More on Texas short term health.

You'll see all kinds of carriers, networks, and plans. We have detailed guides here:

- How to compare Texas Obamacare networks

- How to compare Texas Obamacare carriers

- How to compare Texas Obamacare plans

We even look at small businesses that want to get an employer health plan to have access to PPOs.

Reach out with any questions.