Give us 5 minutes and you might save hours of frustration and maybe even $1000's in health care costs annually.

Sounds over the top but like we said, give us 5 minutes.

It's confusing these days...almost like taxes!

We're going to focus on the individual family market here but we bring the same 25+ years of experience to Medicare and Small Business plans.

First, our credentials:

We've had 10's of 1000's of conversations since 2014 around ACA health plans so we're going run through the common questions in the order we typically get them.

How's that for math!

Let's get a lay of the land with the following knowing that there are dozens of specialized guides if you want to go deeper:

Let's get started.

Much has changed since 2014 with the passage of the ACA law.

The law standardizes the following:

Don't get confused. Some people call saying they don't want Obamacare but it's all the same thing!

The only option outside of this new framework is short term health insurance (see big short term guide).

There are key things to keep in mind with these plans:

We'll use Obamacare throughout the site often only because people understand what that is as opposed to ACA or on-exchange. It's all the same thing.

Don't make this political...our goal is to find you the best plan at the lowest price. Point. Call it whatever you want but don't leave money on the table. That's our theory.

So...let's move on to the next question that comes up.

There are two ways to enroll these days:

Remember, they have the exact same rates, benefits, and networks but there's one huge difference!

Subsidies or Tax-credits (two names for the same thing).

We have a big guide to on versus off-exchange but roughly 99% of our current enrollment is on-exchange.

Found money. Don't lose it. Everything else is the same!

Speaking of found money. People, this is the main show since 2014 and Texans are only recently discovering they've been overpaying for nearly a decade!

Not on our watch!

Here's the quick lay of the land.

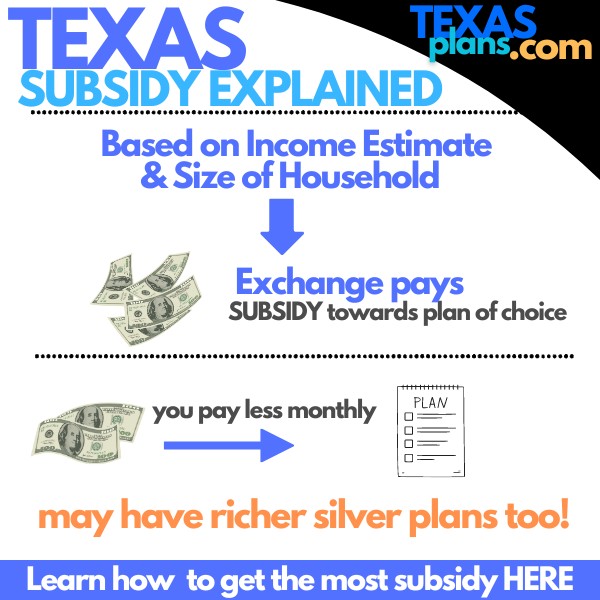

You can qualify for subsidies ON-EXCHANGE based on your income which will reduce your monthly premium right away.

Sometimes down to ZERO! Yes. zero. See it every day with enrollments.

We can only get the subsidy if we enroll on-exchange here. All other things being equal, why enroll off-exchange then?

Not sure. Out of a misinformed notion that they're different. Don't fall for it and reach out with any questions on this.

Our quoting tool will allow you to quote either on or off exchange so no worries. Take our advice though...go on-exchange.

We have big reviews on how to get the most Texas health plan subsidy.

Here's the income chart:

When you run your quote below, two keys to get the best quote:

We have a whole section for self-employed people and Texas health plan subsidy since their situation can be different.

Most of our time these days revolves around tackling the income question since it can be really difficult.

Reach out to us:

Call 800-320-6269

Chat online here

Pick a time to talk here

Once we dial that in, the next question generally revolves around doctors.

If you really want to stay with doctors, this becomes a pressing question on the individual family market.

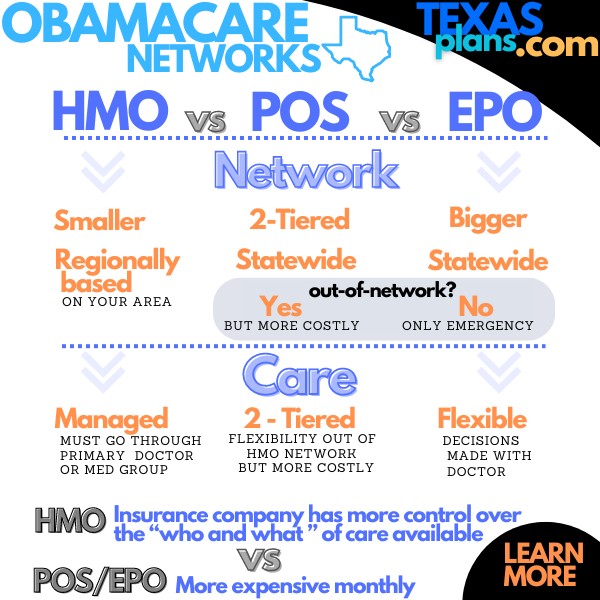

Most of the plans are HMOs these days with a few EPOs sprinkled throughout.

We have a big review on the Texas obamacare networks compared but we make this super easy.

We can't tell you how much time this saves everyone compared to yesteryear where we had to wade through doctor office calls that probably aged us 10 years.

It's all right there for you in the quote!

Once that's out of the way, what plan? This is always the "fun" part of picking a health plan.

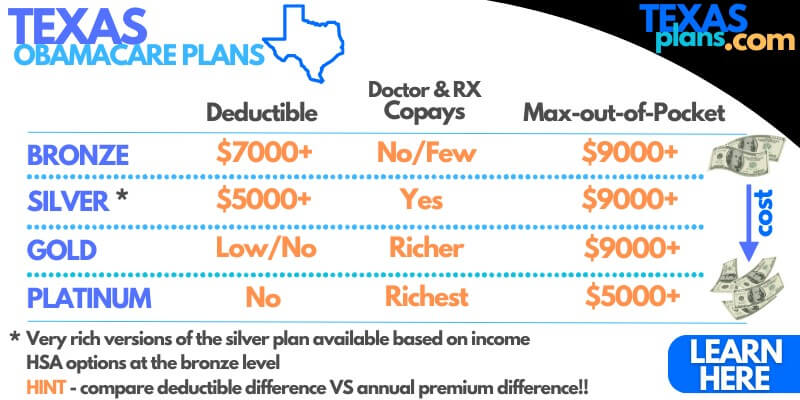

We have a big review on how to compare the Texas health metallic plans but a quick walk through with our top tips.

There are 4 basic levels:

We're happy to walk through since it's Klingon to many people out there.

Here are the top tips:

You'll notice the bronze, silver, and gold all cover the big bill (max out of pocket) the same way.

Is the deductible difference and copays worth the annual premium difference?

We can do all this math for you with the following:

Email us at help@texasplans.com or call 800-320-6269. Even chat online here.

We have break out guides around this here:

Next up, carriers.

The networks (doctor participation) usually drives this decision since it differs by carrier.

First, here are the dominant carriers for Texas individual and family health plans:

You can see how the network really affects popularity of the carriers.

Oscar and Ambetter are basically carried by their EPO plan network which works like a PPO but without benefits out-of-network.

United health is just a powerhouse as the largest carrier in the Nation.

BCBS is a safe bet with their experience directly in the Texas market. If you want more flexibility or control, then Ambetter or Oscar become relevant.

Big comparison of Texas health insurance carriers with more detail.

We even compare the carriers:

No stones left unturned with the rates and networks compared.

Finally, you've seen the magician's secrets. Let's see the rates now!

In line with everything else we do, the quoting tool is free, fast, and easy here:

Remember...

You can quote on or off-exchange but stay with on-exchange. Trust us!

People have all sorts of situations (moving, changing family make-up, income changing, etc).

Reach out to us specifically for your situation. We don't sell. We listen and answer questions.

If you want to work with us (zero cost for our assistance), then great. If not, then be well! Welcome to Texas health insurance. Made easier, we hope.

Call 800-320-6269

Chat online here

Pick a time to talk here